Costs That Vary With the Quantity of Output Produced

Economics questions and answers. Those costs are called a.

Costs Of Production Economics Help

Last month her total output equaled 3000 pounds of clothes.

. A a production expense that changes with the quantity of output produced. Without government intervention negative externalities lead markets to produce a. Variable costs usually change as the firm alters the quantity of output produced.

Variable costs are question 8 options. Are constant over the short-run regardless of the quantity of output produced. Those costs are called a.

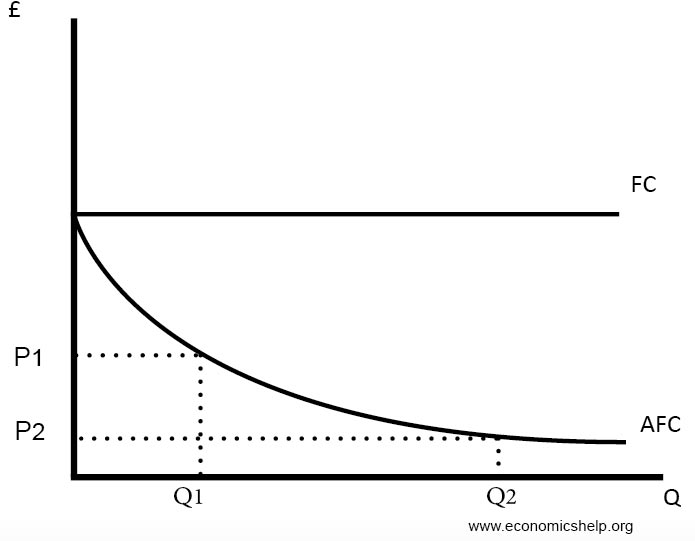

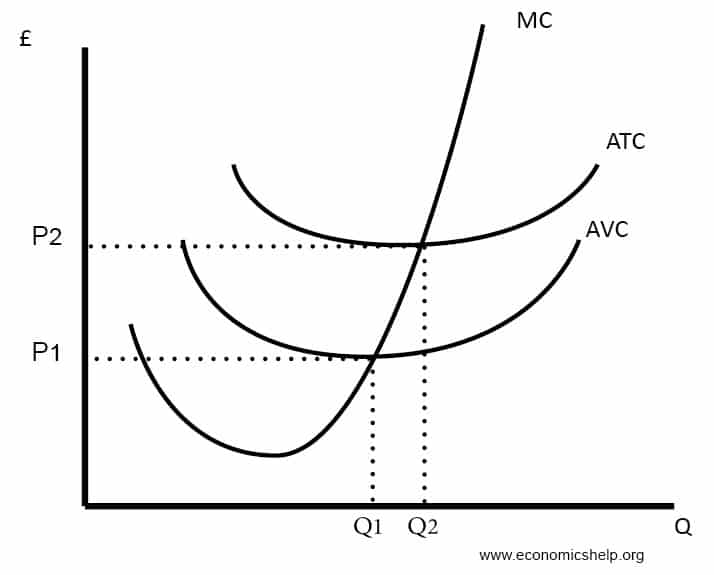

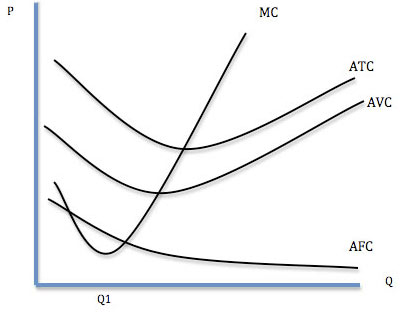

Variable cost divided by the quantity of output. The accompanying table shows three possible combinations of fixed cost and average variable cost. Average variable cost is equal to.

For each of the three choices calculate the average total cost of. Those costs are called a. Some costs do not vary with the quantity of output produced.

O c fixed costs. Which type of cost is does NOT change as the quantity of output produced changes. Economies of scale arise when.

Those costs are called a. O c fixed costs. If the production volume is zero then no variable costs are incurred.

Price x quantity - total cost. ATC change in total cost change in. Examples of variable costs include sales commissions.

Change as a function of the next unit of output produced D. Those costs are called a. Quantity of output and total cost.

For a given time period are constant no matter the quantity of output produced C. A cost that does not depend on the quantity of output produced is called a. Fixed cost divided by the quantity of output.

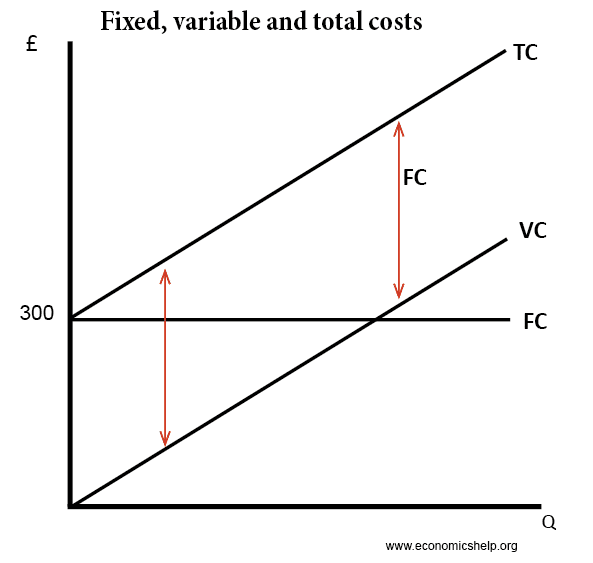

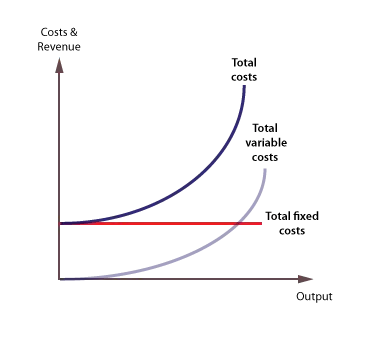

Variable costs are costs that change with the changes in the level of production. When a manu- facturer increases output there will be increased costs with output for variables such as labor materials and shipping costs. - the relationship between quantity produced and total costs.

O c fixed costs. Are defined as the change in total costs when one more unit of output is produced. Variable costs are costs that do vary with output and they are also called direct costs.

Are subtracted from sales to compute the contribution margin. Those costs are called a. Costs that vary directly with the level of production.

Examples of typical variable costs include fuel raw materials and some labour costs. Variable cost divided by change in quantity produced is a. Costs that do not vary with the quantity of output produced.

Some costs do not vary with the quantity of output produced. Change as a small quantity of output produced changes. C equal to total cost divided by the units of output produced.

As more units are produced the total variable costs increase. O a total cost O b. This means her average fixed cost ________ by a little more than ________.

Which type of cost is does NOT change as the quantity of output produced changes. D a production expense that does not vary with output. Some costs do not vary with the quantity of output produced.

B the amount by which a firms cost changes if the firm produces one more unit of output. Fixed and variable costs. An economy is self-sufficient in production.

Marginal cost equals a. 1 See answer Advertisement. Greater than efficient output levels and positive externalities lead markets to produce smaller than efficient.

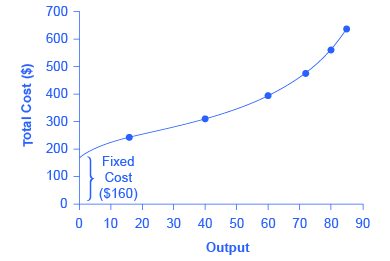

They are also called overheads. Fixed costs are large relative to variable costs. For example once a particular plant size is decided upon the lease on the factory is a fixed cost since the rent doesnt change depending on.

Variable and fixed costs. Companies incur two types of production costs. This month her total output fell to 2700 pounds.

Variable costs change based on the amount of output produced. Average cost Clear my choice. Economics questions and answers.

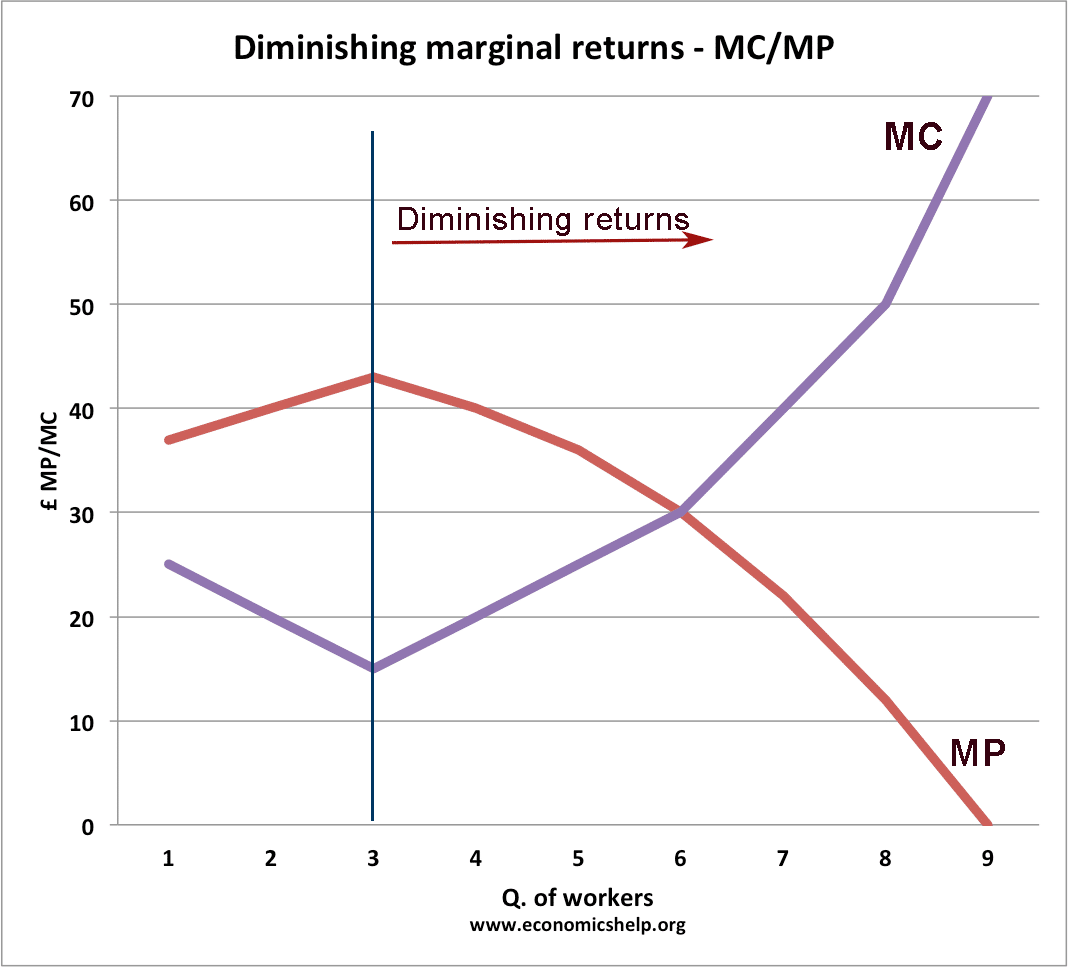

Marginal costs are costs that do not vary with the quantity of output produced. Change as a function of the quantity of output produced B. False marginal costs change as output changes.

Some costs do not vary with the quantity of output produced. - gets steeper as the quantity of output increases because of diminishing marginal product. Those costs are called - 9400832 bammbamm1307 bammbamm1307 03292018 Business High School answered Some costs do not vary with the quantity of output produced.

None of the above are correct. Costs that do not change when the quantity of output produced changes. None of the above are correct.

Comprise the sum total of all production expenses of the firm for some. Fixed cost O d. ATC change in total cost change in quantity of input.

Average total cost ATC is calculated as follows. Average variable cost is constant in this example it does not vary with the quantity of output produced. That is they rise as the production volume increases and decrease as the production volume decreases.

Variable costs are costs that vary directly with the amount of output. Some costs do not vary with the quantity of output produced. Fixed costs are upfront costs that dont change depending on the quantity of output produced.

Total cost divided by quantity of output produced. Some costs do not vary with the quantity of output produced. Fixed costs are those that do not vary with output and typically include rents insurance depreciation set-up costs and normal profit.

Individuals in a society are self-sufficient. ATC total cost quantity of output. Variable costs may include labor commissions and raw materials.

A fell. Fixed costs variable costs. The market value of all the inputs a firm uses in production.

Comprise the sum total of all production expenses of the firm for some time period E. Quantity of inputs and total cost.

Cost Output Relationship In Short Run Long Run Cost Curves

Costs Of Production Maple Help

Costs Of Production Economics Help

Types Of Costs Economics Help

The Structure Of Costs In The Short Run Article Khan Academy

Costs Of Production Economics Help

Costs

Costs Of Production Economics Help

Costs Revenue Profits Learn Economics

No comments for "Costs That Vary With the Quantity of Output Produced"

Post a Comment